New Starts - No Pickup In Sight, A Structural Change

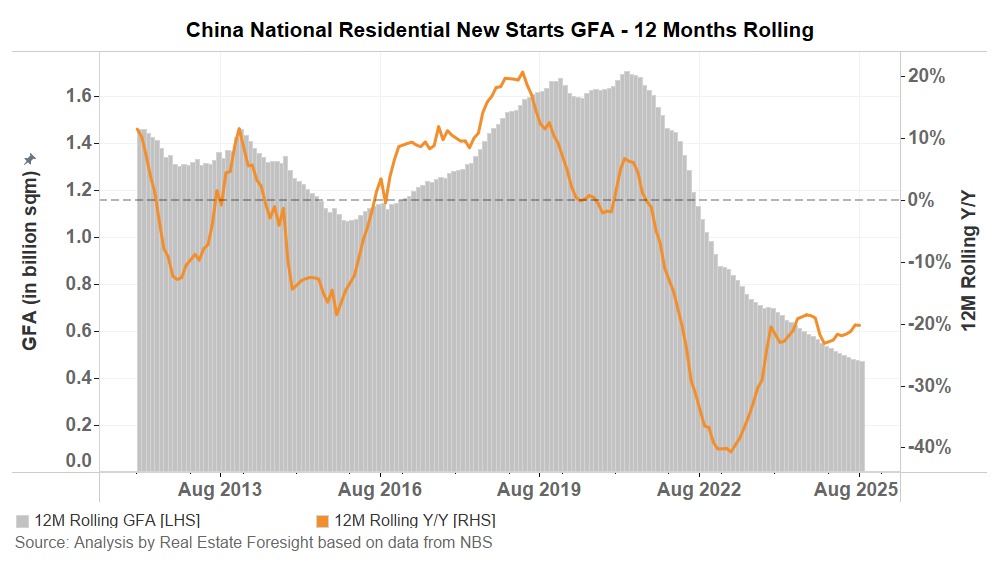

China's residential new starts in Gross Floor Area at the national level (as per the official statistics from NBS) are now (August 2025 data) down over 70% from the peak in March 2021 in terms of the 12-month rolling measure, with the pace of decline staying at -23% to -20% in 2025:

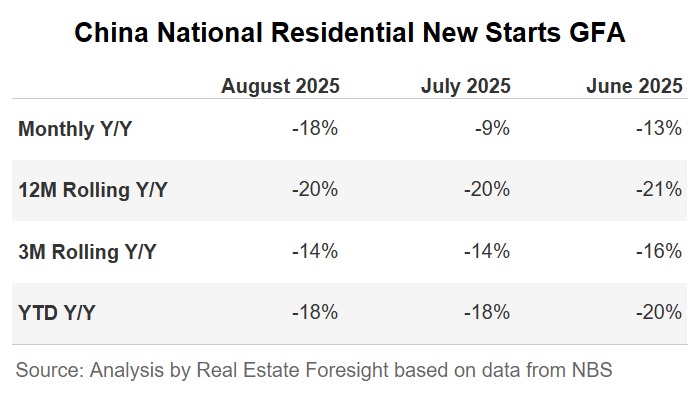

Like with many measures, it's worth looking at multiple-period metrics, but here the picture is pretty much the same:

This decline in new starts reflects the market downturn that began in 2021, accompanied by a further policy shift towards the utilisation of existing projects, as seen in the push for urban village renovations across major cities, and the development of 'quality housing'.

The 'quantity to quality shift' theme also shows in the land markets, where developers buy more land in terms of value but less in terms of GFA. Land acquisitions across 300 cities were up +16% YTD y/y in terms of RMB but down -10% in terms of GFA (based on the data from China Index Academy, for Jan-Aug 2025). The land acquisitions are mainly by the State Owned Enterprises (SOEs), though, as the private developers continue to struggle and have to focus on the delivery of the pre-sold homes.

The structural drop in new starts should translate into a lower demand for steel and related commodities, though the push for completions (i.e. accelerating/starting construction of what was already pre-sold) has provided some support for the demand in the meantime.

Previous Notes:

#2 China Property Signals: Watching the 'Whitelist Figures'

#1 China Property Signals: 'Completed-not-Sold' Inventory on the Rise

For more about China housing research, visit Real Estate Foresight.